FIRE

Welcome to “Fire” on LiveTheLife.TV, your ultimate destination for cutting-edge insights and inspiration in the realms of art, technology, and lifestyle. Here, we ignite your passion for creativity and innovation with curated content that spans from groundbreaking digital art and immersive experiences to the latest trends in technology and beyond. Join us as we explore the intersection of art and tech, celebrating the visionaries who are pushing boundaries and redefining the future. Dive into our stories, get inspired, and live the life you’ve always envisioned.

LIVETHELIFETV

LIVETHELIFETV

Achieving financial independence and early retirement (FIRE) is more than just escaping the 9-to-5 grind; it’s about embracing a life filled with freedom, balance, and purpose. When you’re financially independent, you have the liberty to pursue your passions and hobbies without the constraints of a demanding job. This freedom allows you to prioritize your mental and physical health, ensuring you live a life without compromise. You can spend quality time with family and friends, fostering strong, meaningful relationships and creating lasting memories. With a balanced work-life schedule, you have the flexibility to mentor and inspire others, say no to projects that don’t align with your values, and take time for personal growth and continuous learning. Financial independence grants you the ability to contribute actively to your community, engage in creative pursuits, and support causes you believe in, all while enjoying a peaceful, stress-free environment. This journey not only enhances your well-being but also allows you to live authentically, practice gratitude, and savor life’s moments fully. By prioritizing experiences over possessions, you can travel, explore new cultures, and wake up each day excited about the opportunities ahead. Ultimately, FIRE enables you to live a life true to yourself, filled with joy, contentment, and a deep sense of fulfillment.

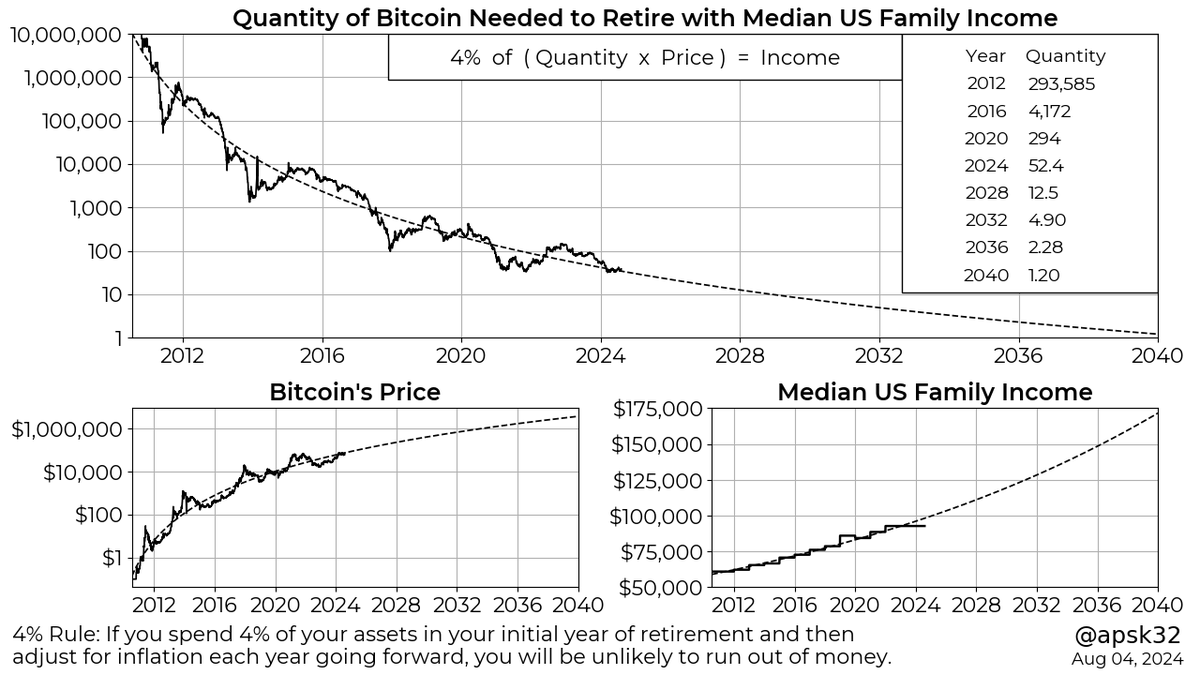

How Much Do You Need to Retire? It depends!

One sunny afternoon, John sat by the pool of his fully paid-off home in Costa Rica, sipping his favorite coffee. As he watched the palm trees sway gently in the breeze, he realized something profound. Financial freedom had shifted his priorities. No longer consumed by the need to chase money, he found joy in the simple pleasures of life—spending time with family, traveling, and enjoying leisurely mornings without the stress of business decisions weighing on his mind.

John’s friend, Sarah, had a different perspective. Her ultimate life goal was to generate 5% annually from her $2.4 million portfolio, providing her with $10,000 a month. This amount was perfect for her as it allowed her to live comfortably almost anywhere in the world and still save a good portion. Sarah admired John’s poolside lifestyle and aspired to achieve the same level of tranquility.

John knew that $5 million meant never flying coach again, while $10 million could afford him shorter private flights and first-class international trips on airlines like Etihad or Emirates. With $100 million, he could charter a G650 for long-haul flights. As John sat by his pool, he reflected on his journey. He no longer needed to be driven by the relentless pursuit of wealth. He had reached a point where financial freedom allowed him to enjoy life without compromise. The sun set over his tropical villa, casting a golden hue over the water, and John knew he had made the right choice. Financial freedom meant different things to different people, but for John, it was about peace, joy, and the ability to live the good life.

Initial Calculation

- Initial Values:

- Initial BTC holding: 21 BTC

- Initial BTC price: $60,000

- Initial net worth: $1,260,000

- Annual cost of living: $50,000

- Annual withdrawal rate: 4%

- Annual Withdrawal (4% Rule):

- 4% of $1,260,000 = $50,400 per year

Year-by-Year Projection with 15% BTC Growth

BTC price, portfolio value, and the surplus for each of the next 30 years.

Yearly Breakdown

| Year | BTC Price ($) | Portfolio Value ($) | 4% Withdrawal ($) | Cost of Living ($) | Surplus/Shortfall ($) | Remaining BTC |

|---|---|---|---|---|---|---|

| 2024 | 60,000 | 1,260,000 | 50,400 | 50,000 | 400 | 21.00 |

| 2025 | 69,000 | 1,449,000 | 57,960 | 50,000 | 7,960 | 21.00 |

| 2026 | 79,350 | 1,666,350 | 66,654 | 50,000 | 16,654 | 21.00 |

| 2027 | 91,253 | 1,916,313 | 76,652.52 | 50,000 | 26,652.52 | 21.00 |

| 2028 | 104,940 | 2,203,740 | 88,149.60 | 50,000 | 38,149.60 | 21.00 |

| 2029 | 120,681 | 2,534,301 | 101,372.04 | 50,000 | 51,372.04 | 21.00 |

| 2030 | 138,783 | 2,913,063 | 116,522.52 | 50,000 | 66,522.52 | 21.00 |

| 2031 | 159,600 | 3,345,600 | 133,824 | 50,000 | 83,824 | 21.00 |

| 2032 | 183,540 | 3,854,340 | 154,173.60 | 50,000 | 104,173.60 | 21.00 |

| 2033 | 211,071 | 4,432,491 | 177,299.64 | 50,000 | 127,299.64 | 21.00 |

| 2034 | 242,732 | 5,095,365 | 203,814.60 | 50,000 | 153,814.60 | 21.00 |

| 2035 | 279,142 | 5,857,792 | 234,311.68 | 50,000 | 184,311.68 | 21.00 |

| 2036 | 321,013 | 6,735,461 | 269,418.44 | 50,000 | 219,418.44 | 21.00 |

| 2037 | 369,165 | 7,744,780 | 309,791.20 | 50,000 | 259,791.20 | 21.00 |

| 2038 | 424,540 | 8,903,336 | 356,133.44 | 50,000 | 306,133.44 | 21.00 |

| 2039 | 488,221 | 10,230,637 | 409,225.48 | 50,000 | 359,225.48 | 21.00 |

| 2040 | 561,454 | 11,748,219 | 469,928.76 | 50,000 | 419,928.76 | 21.00 |

| 2041 | 645,672 | 13,480,956 | 539,238.24 | 50,000 | 489,238.24 | 21.00 |

| 2042 | 742,523 | 15,457,099 | 618,283.96 | 50,000 | 568,283.96 | 21.00 |

| 2043 | 853,901 | 17,708,664 | 708,346.56 | 50,000 | 658,346.56 | 21.00 |

| 2044 | 981,986 | 20,271,964 | 810,878.56 | 50,000 | 760,878.56 | 21.00 |

| 2045 | 1,129,284 | 23,188,959 | 927,558.36 | 50,000 | 877,558.36 | 21.00 |

| 2046 | 1,298,676 | 26,507,303 | 1,060,292.12 | 50,000 | 1,010,292.12 | 21.00 |

| 2047 | 1,493,477 | 30,280,628 | 1,211,225.12 | 50,000 | 1,161,225.12 | 21.00 |

| 2048 | 1,717,499 | 34,568,722 | 1,382,748.88 | 50,000 | 1,332,748.88 | 21.00 |

| 2049 | 1,975,124 | 39,438,168 | 1,577,526.72 | 50,000 | 1,527,526.72 | 21.00 |

| 2050 | 2,271,393 | 44,963,893 | 1,798,555.72 | 50,000 | 1,748,555.72 | 21.00 |

| 2051 | 2,612,102 | 51,229,477 | 2,049,179.08 | 50,000 | 1,999,179.08 | 21.00 |

| 2052 | 3,003,917 | 58,328,898 | 2,333,155.92 | 50,000 | 2,283,155.92 | 21.00 |

| 2053 | 3,454,505 | 66,367,233 | 2,654,689.32 | 50,000 | 2,604,689.32 | 21.00 |

Conclusion

With a cost of living of $50K / year and a 15% annual growth rate over 30 years:

- The portfolio value increases from $1,2M to approximately $66M.

- The annual withdrawal amount grows to $2,6M in 2053.

- Your BTC holdings remain at 21 BTC throughout the period.

This model demonstrates that under these assumptions, your retirement plan is highly sustainable, and you will accumulate a considerable surplus each year, allowing for a very comfortable and financially secure retirement. #FIRE

With a 20% annual growth rate in BTC over 30 years:

• The portfolio value increases to approximately $249M by 2053.

• The annual withdrawal amount grows to $9M in 2053.

With a 25% annual growth rate in BTC over 30 years:

• The portfolio increases significantly, reaching approximately $804M by 2053.

• The annual withdrawal amount grows to $32M in 2053.

Data from CoinGecko shows that Bitcoin has seen considerable year-on-year increases over longer periods, averaging a 25% year-on-year increase from 2014 to 2023. This consistent growth underscores Bitcoin's historical performance as a high-growth asset, though past performance does not guarantee future results.

Bear Scenario ($3 million by 2045): Annual growth of 22%.

Base Scenario ($13 million by 2045): Annual growth rate of 26%.

Bull Scenario ($50 million by 2045): Annual growth rate of 34%.

PlanB

Assuming Bitcoin only increases to $130,000 by 2042 (VanEck)

• The annual growth rate needed is approximately 4%.

• By 2042, your portfolio would be approximately $2,6M.

• With a 6.9% withdrawal rate, you can spend $186K per year in 2042.

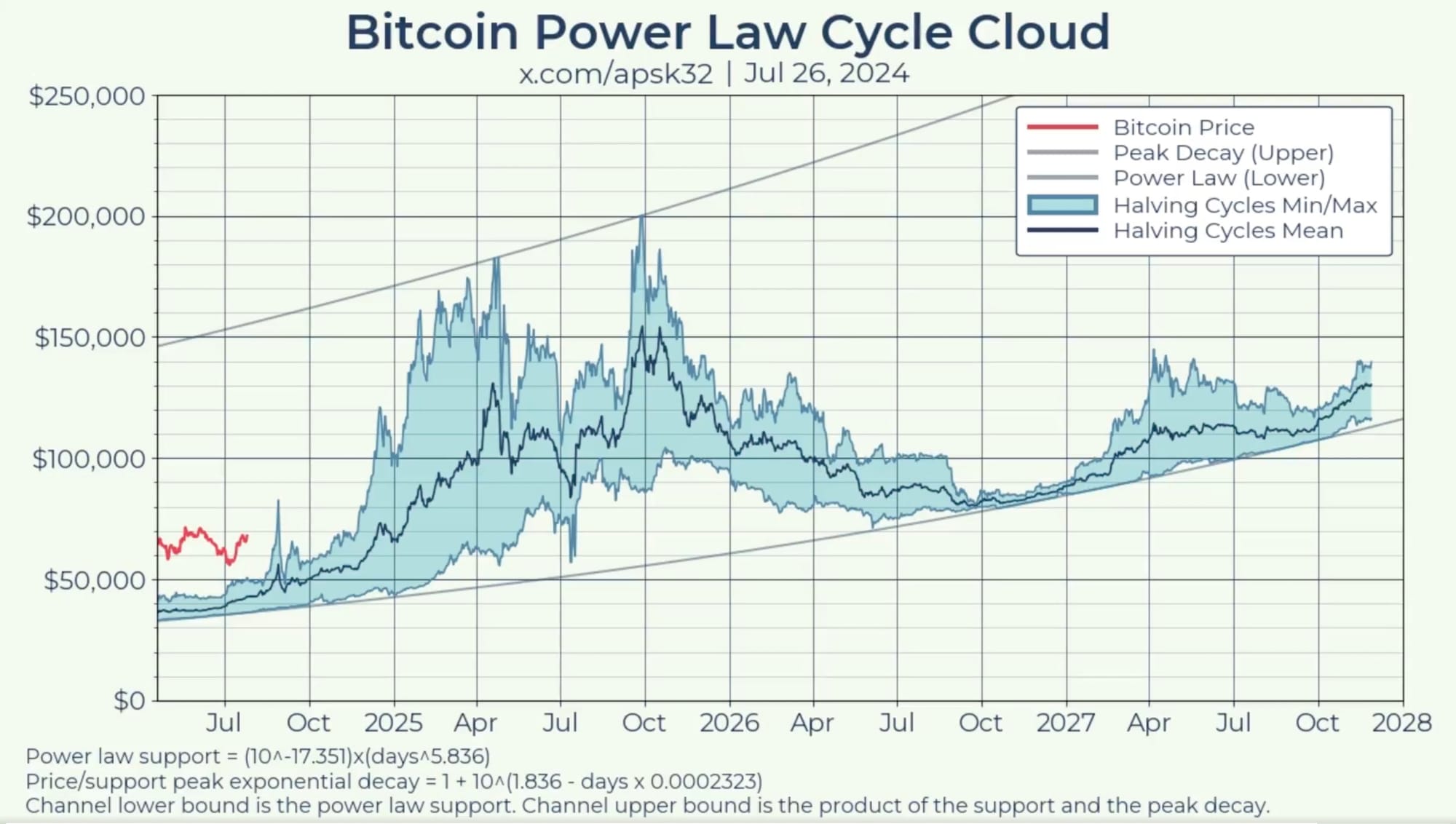

Source: x.com/apsk32

Real Estate Median Sales Price / BTC

Over the past decade, housing prices have increased by 50%, while wages have only risen by 20%. While the true inflation rate is debatable, government data suggests a cumulative inflation rate of 33%. This discrepancy is more pronounced in major cities, highlighting the financial pressures faced by the upper middle class. For more detailed insights, you can read the full article here.