The example follows a musician that launches their debut album. In order to listen to the album & all subsequent works, a user needs to acquire a token of the artist and show that they are holding it.

In order to buy this token (say: artistToken), the user spends ETH. The largest percentage of the ETH that is spent to buy the artistToken is kept in a communal pool with a small percentage of the ETH being sent as revenue to the artist. When the user does not want to listen to the music anymore, they can sell their artistToken, and get some ETH back from the communal pool. This artistToken that is sold is then removed from circulation.

The ETH cost to buy the artistToken & the ETH the user receives when selling their artistToken is determined by how many tokens are in circulation. As more tokens are in circulation, the larger the communal pool is. There is a correlation between the amount of tokens in circulation and the amount of users who want to listen to the music. A user can however buy a token & not use it to access the media (for whatever reason).

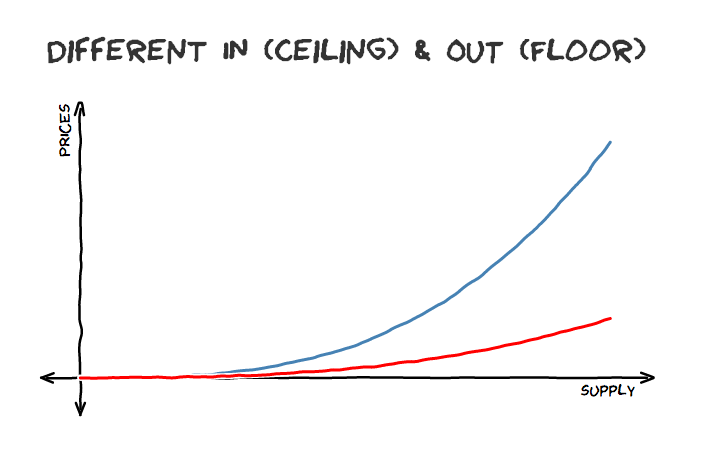

This cost to buy & sell is plotted on a specific, hardcoded curve. Different curves (exponential, linear or sigmoid) have different around outcomes on how token buyers view their commitments.

Over time thus, the price will increase & decrease along this curve in order to consume the media as users buy & sell their artistTokens. The supply of tokens will thus grow and shrink relative to the amount of people who want to listen to the music.

Users who buy an artistToken early receives a benefit for being an early adopter if they choose to exit & sell their artistToken when the popularity has increased & the amount of tokens in supply & the size of the communal pool has done so similarly.

Equally, a user who buys an artistToken at the peak of the song’s popularity and sells it back at at a time when there’s less outstanding supply, will get less ETH back than when they bought access.

Second Order Benefits: Fan-Artist Connections, Early Adopter Benefits & Curation

By requiring a token to get access to the media in this manner allows various second-order benefits.

1) A musician has direct access to their fans who have committed to listen to their music.

The token holders are the true fans who aren’t pirating the music elsewhere. The musician can offer various benefits to the token holders above & beyond media access. For example, if it costs say, 1 artistToken to listen to the music, they can offer higher tier rewards, such as:

1 artistToken == access to discography.

100 artistTokens == access to bonus content & media.

1000 artistTokens == access to an encrypted, fan-only communication forum.

10000 artistTokens == access to meet & greets in cities where the musician is playing.

2) Early Adopter Benefits & Curatorial Markets

If more media is consumed in a similar manner, curators can be rewarded for surfacing novel content by undergoing opportunity cost by staking their ETH towards various forms of media. Thus early adopters of popular media (across all media) get rewarded & in turn allow others to find novel media to consume. They are being rewarded for doing the job curating through skin-in-the-game.

Optional Platform Revenue:

As with CryptoKitties, it is not necessary on a protocol level to leverage a fee. In CryptoKitties case, they can be traded/bought/sold through other means, but if done through the CryptoKitties website they *do* charge a fee.

Similarly, Ujo can charge a similar fee if tokens are bought/purchased through Ujo & thus it allows Ujo to earn revenue from the economic activity taking place.

Reliance:

At this stage, a centralized provider is required to check if whomever is accessing the content has the required amount of tokens. Potentially in the future, the encryption/decryption & file serving can be done automatically without requiring a centralized provider. Additional cryptographic research can be done here.

As is the case with emergent outcomes, anyone can optionally choose to give access to media to anyone with a token, and thus it’s possible that anyone can become a media provider with consent of the musician.

Website: ujomusic.com

Read More

Felipe Gaúcho Pereira

Felipe Gaúcho Pereira billy rennekamp

billy rennekamp Simon de la Rouviere

Simon de la Rouviere Simon de la Rouviere

Simon de la Rouviere